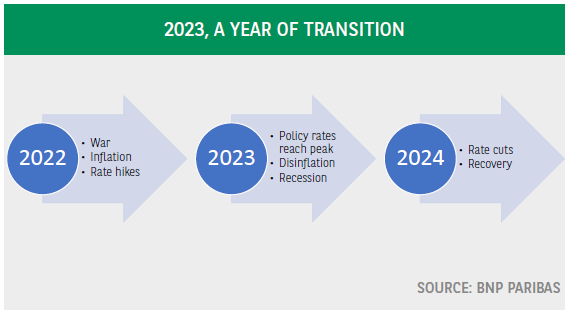

2022 was a year of profound transformation, of shifting geopolitical and economic paradigms. Looking ahead, 2023 should see a change of direction in key economic variables. Headline inflation should decline significantly, central bank rates should reach their cyclical peak and the US and the euro area should spend part of the year in recession. 2023 can be considered as a year of transition, paving the way for more disinflation, gradual rate cuts and a soft recovery in 2024.

The traditional year-end reviews have reminded us of the exceptional nature of the past year: the war in Ukraine, the energy and food price shock, huge labour market bottlenecks, inflation reaching a multiple of what central banks are targeting, thereby triggering a ‘whatever it costs’ approach to monetary tightening, etc.

2022 was a year of profound transformation, of shifting paradigms, not only geopolitically but also economically. Looking ahead, 2023 should see a change of direction in key economic variables. Headline inflation should decline significantly, largely due to favourable base effects and an easing of supply pressures. Central bank rates should reach their cyclical peak. Initially, the Federal Reserve and the ECB should continue hiking their policy rates, but subsequently -probably in spring- their monetary stance should be sufficiently tight, allowing them to switch to a wait-and-see attitude and monitor how the economy is reacting to past hikes, before deciding on the next step.

Finally, the US and the euro area should spend part of the year in recession. This can be considered as the price to be paid to bring inflation back under control through tight monetary policy. Recessions are disinflationary because subdued demand reduces the pricing power of companies and slows down wage growth.

It means that 2023 can be considered as a year of transition, paving the way for a gradual normalization in 2024. Normalization in terms of a significant narrowing of the gap between observed and target inflation, enabling central banks to start cutting interest rates, probably in the first half of 2024. This prospect should support investor risk appetite and boost confidence of households and firms, thereby contributing to the economic recovery.

Although these broad trends look like very likely, the devil is in the detail. The transition in 2023 might be bumpier than expected. The base scenario is for a short and shallow recession because of several factors of resilience1 but the contraction might be bigger than anticipated.

Possible causes could be a new, significant and lasting increase in the price of gas or a slower than expected decline in inflation, which could fuel concerns of interest rates moving higher, thereby hitting demand. Past rate hikes could also have a bigger than expected impact, particularly on the housing market and credit conditions.

Another issue concerns the normalization in 2024: how will it look like? The question matters because expectations about the nature of the recovery will influence decisions by firms and households this year. The list of recovery drivers is long2, but we nevertheless expect the recovery to be soft for at least two reasons. Traditionally, central banks cut interest rates aggressively as the economy enters a recession, but in this cycle inflation will still be too high. Rate cuts should come later and be more gradual than normal due to the slow decline in core inflation. This means less of a boost to final demand. Another factor is labour hoarding. Companies have been struggling to fill vacancies, which will probably make them reluctant to lay off staff during a recession3. However, this also would imply a slow increase in employment during the recovery.

Download The Full Eco Flash

previous

previous