A recession has started, but what will it look like?

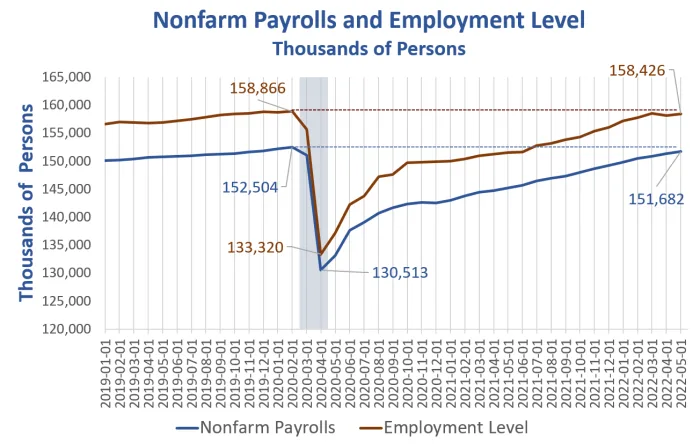

Nonfarm Payrolls and Employment Levels from BLS, chart by Mish

Despite fantasy soft landing theories by the Fed, president Biden, and Treasury Secretary Janet Yellen, a Recession Has Clearly Started

Some say it's too early to make the call and jobs are too strong. Others say it takes two quarters of negative GDP.

However, it doesn't take two quarters of negative GDP. The NBER is the official arbiter of recessions and the committee looks at a variety of factors.

The NBER's definition emphasizes that a recession involves a significant decline in economic activity that is spread across the economy and lasts more than a few months. In our interpretation of this definition, we treat the three criteria—depth, diffusion, and duration—as somewhat interchangeable. That is, while each criterion needs to be met individually to some degree, extreme conditions revealed by one criterion may partially offset weaker indications from another. For example, in the case of the February 2020 peak in economic activity, the committee concluded that the subsequent drop in activity had been so great and so widely diffused throughout the economy that, even if it proved to be quite brief, the downturn should be classified as a recession.

Q: The financial press often states the definition of a recession as two consecutive quarters of decline in real GDP. How does that relate to the NBER's recession dates?

A: Most of the recessions identified by our procedures do consist of two or more consecutive quarters of declining real GDP, but not all of them. In 2001, for example, the recession did not include two consecutive quarters of decline in real GDP. In the recession from the peak in December 2007 to the trough in June 2009, real GDP declined in the first, third, and fourth quarters of 2008 and in the first and second quarters of 2009. Real GDI declined for the final three quarters of 2001 and for five of the six quarters in the 2007–2009 recession.

In 2001, GDP didn’t contract for two consecutive quarters, but the NBER labeled it a recession anyway. In 2020, the recession was over in two months.

Expect Minimal Rise in Unemployment

Jobs are a lagging indicator but there are many reasons to expect a minimal rise in unemployment.

The lead chart offers a clue why. The economy still has not recovered all of the jobs lost from the 2020 recession.

While technology is shedding jobs, the leisure and hospitality sector still begs for employees.

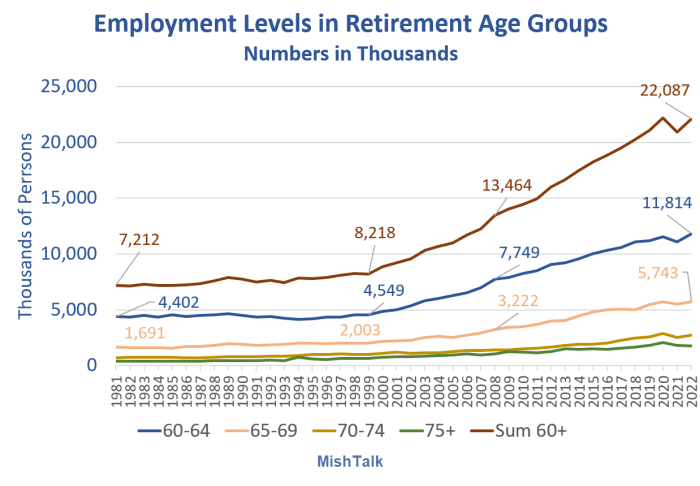

Meanwhile, the potential for Boomers to retire is very high and rising.

Employment Levels in Retirement Age Groups

Age 60+ Employment

- In 2022: 22.09 Million

- In 2008: 13.46 Million

- In 1999: 8.22 Million

- In 1981: 7.21 Million

There are over 22 million people age 60 or over who are still working. We have never seen anything like this before, so don't expect prior recessions to be a model for this one.

Millions of these people will retire. Employment may drop substantially when these boomers and Gen X employees retire, but falling employment and rising unemployment are not the same thing in the Fed's eyes.

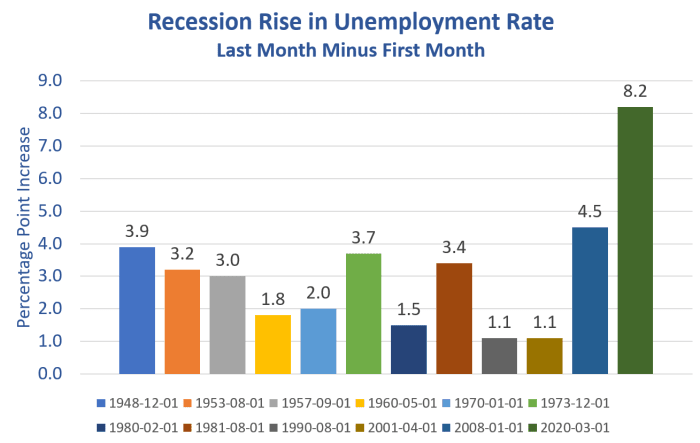

Rise in Unemployment Rate

Rise in Unemployment Rate Key Points

- In 12 previous recessions, the lowest rise in unemployment was in 1990 and 2001, 1.1 percent each.

- The highest jump was 8.2 percent in 2020 and that was undoubtedly understated.

Given the pending levels of retirement and the incomplete jobs recovery from the 2020 recession, I expect this to be a very weak recession in terms of rising unemployment.

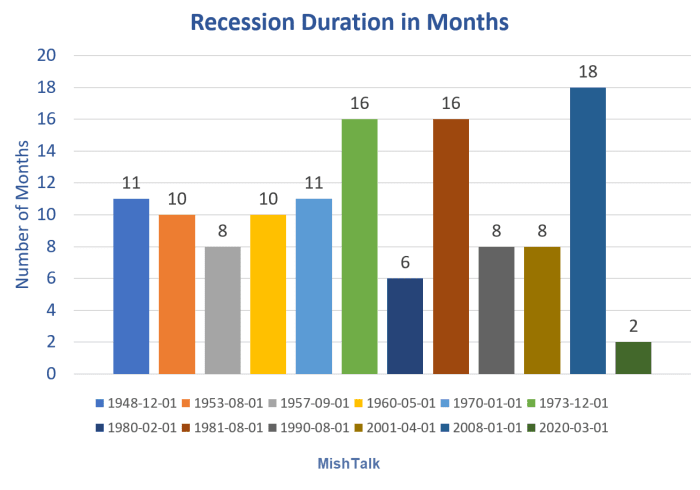

Recession Duration in Months

Recession Duration Key Points

- The 2020 recession only lasted 2 months.

- The 2008 recession lasted 18 months.

Expect Shallow and Long

I see no use in averaging the above recession jambalaya. Instead, I expect the opposite of the 2020 recession.

2020 was very short and unprecedented steep. 2022 will be the opposite, perhaps unprecedented shallow from an unemployment standpoint.

Fed's Hands Are Tied

The Jobs data speaks for itself. That is half of the Fed's mandate. If jobs stay relatively strong as I expect, the Fed will have met that half of its mandate.

The Fed's other mandate is price stability. Everyone on the planet knows the Fed flunked. It gets grade F.

The Fed does not want another grade F. It will err on the side of caution unless there is a credit event or a collapse in jobs.

Powell: “We understand better how little we understand about inflation”

Let's review Powell's comments at the June 29 ECB economic forum: Powell: “We understand better how little we understand about inflation”

- Powell: “There’s a clock running here. The risk is that because of the multiplicity of shocks, you start to transition into a higher-inflation regime. Our job is literally to prevent that from happening, and we will prevent that from happening.”

- Powell: “The process is highly likely to involve some pain, but the worse pain would be in failing to address this high inflation and allowing it to become persistent.”

- Powell: “Households are in very strong financial shape. They still have a lot of excess savings from forced savings and also fiscal transfers. The same is true of businesses. The labor market is tremendously strong. Overall the US economy is well positioned to stand tighter monetary policy.”

- Powell: “Is there a risk we would go too far? Certainly there’s a risk. The bigger mistake to make, let’s put it that way, would be to fail to restore price stability.”

I strongly disagree with point three except for the labor market. The other points could not possibly be more clear, even if I do not necessary agree.

Inflation Expectations

Point #1 above is related to the idea that inflation expectations might get out of hand.

The concept is ridiculous as discussed on June 25 in The Asininity of Inflation Expectations, Once Again By Powell and the Fed.

However, Powell's position is clear: “Our job is literally to prevent that from happening, and we will prevent that from happening.”

“The bigger mistake to make, let’s put it that way, would be to fail to restore price stability.”

Expect an Overshoot

Based on Powell's comments. I expect the Fed to overshoot.

Then, unless the jobs picture or credit markets go haywire, Powell will be very reluctant to step on the gas out of fear of creating another inflation cycle.

Flashback June 26, 2021

Just over a year ago, I commented Fed Will Foolishly Continue QE Purchases in Search of Higher Inflation

Here are some FOMC Statements

- The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With inflation having run persistently below this longer-run goal, the Committee will aim to achieve inflation moderately above 2 percent for some time so that inflation averages 2 percent over time and longer‑term inflation expectations remain well anchored at 2 percent. The Committee expects to maintain an accommodative stance of monetary policy until these outcomes are achieved.

- The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.

- In addition, the Federal Reserve will continue to increase its holdings of Treasury securities by at least $80 billion per month and of agency mortgage‑backed securities by at least $40 billion per month until substantial further progress has been made toward the Committee's maximum employment and price stability goals.

My June 26, 2021 Comments

The Fed either has no idea inflation is roaring if one accurately includes home prices, or it simply does not care. My take is the Fed is basically clueless.

What are the Fed and Congress going to do next with stimulus wearing off and banks choking on the Fed's QE already?

Looking ahead, the fourth quarter and 2022 GDP and will be much weaker than most expect.

The irony in the Fed's actions is they are indeed increasing inflation, but only in the most unproductive, yet uncounted ways. There's plenty of inflation now, just not as they measure it.

And when bubbles burst, expect another painful round of asset deflation, likely accompanied by the price deflation they fear.

I accidentally ran into that post yesterday while looking for something else. I then made a few Tweets about it.

Inflation of Deflation?

We will have another round of asset deflation, in fact, it's started.

Whether that leads to CPI-measured inflation is another question. But if you properly throw housing into the equation it sure seems likely.

Regardless, It's asset-price deflation that matters, not routine CPI-price deflation.

Historical Perspective on CPI Deflations: How Damaging are They?

Please see Historical Perspective on CPI Deflations: How Damaging are They?

A BIS study concluded “Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive.”

BIS: “Once we control for persistent asset price deflations, persistent goods and services (CPI ) deflations do not appear to be linked in a statistically significant way with slower growth even in the interwar period.”

Here We Go Again

The central bank battle against routine and beneficial CPI deflation has once again created another set of bubbles.

Those bubbles are bursting now, causing very asset bubble deflation that central banks ought to have feared in the first place.

No White Hats

There will be no Fed posse to the rescue this time. For four decades the Fed had disinflationary winds of globalization at it back. It could easily step on the gas without starting an inflation spiral.

That changed in 2020. The Fed now has inflationary winds of de-globalization and wars blowing in its face. Labor pressures also remain inflationary.

The Fed knows it made a mistake and will be very reluctant to repeat it.

What About the Stock Market?

Look at things this way: We have energy shocks, wage pressures, a supply chain mess, earnings estimates that remain ridiculously high, and a Fed that is likely to overshoot. Don't expect the Fed to come to the rescue.

Finally, we have an inept president pushing unions and promoting clean energy policies that are very inflationary.

Even if the recession isn't long, this is a very nasty brew. The economy rates to be weak, perhaps flirting with recession for a long time.

So expect a disaster in the stock market. We are not close to the bottom.

previous

previous