The S&P US Composite PMI™ shows a steep decline in business activity in August.

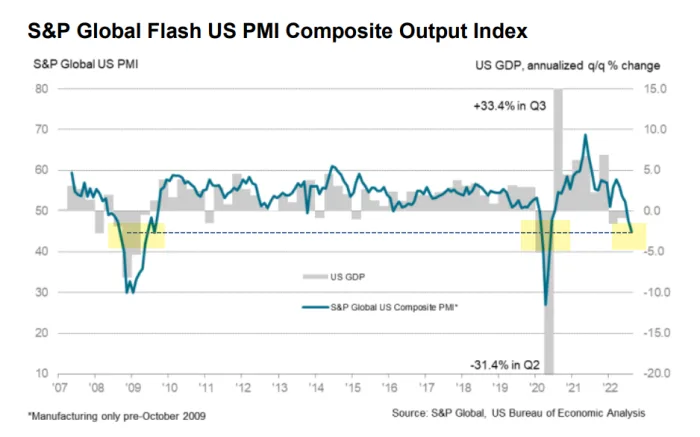

Global Flash PMI courtesy of S&P. Yellow highlights and dashed line added.

Faster Fall in US Private Sector Output Amid Weak Client Demand

The S&P reports a Faster Fall in US Private Sector Output Amid Weak Client Demand

- Flash US PMI Composite Output Index at 45.0 (July: 47.7). 27-month low.

- Flash US Services Business Activity Index at 44.1 (July: 47.3). 27-month low.

- Flash US Manufacturing Output Index at 49.3 (July: 49.5). 26-month low.

- Flash US Manufacturing PMI at 51.3 (July: 52.2) 25-month low.

Sharp Decline

US private sector firms signaled a sharper fall in business activity during August, according to latest ‘flash’ PMI™ data from S&P Global. The decrease in output was the fastest seen since May 2020 and solid overall. The rate of contraction also outpaced anything recorded outside of the initial pandemic outbreak since the series began nearly 13- years ago.

Though modest, the drop in new orders was the sharpest in over two years. New sales were weighed down by weak domestic and foreign client demand, as new export orders fell further and at a solid pace.

The rate of input cost inflation eased for the third month running midway through the third quarter, with input prices rising at the slowest pace for a year-and-a-half. That said, the pace of increase in operating expenses remained historically marked, with firms linking hikes in cost burdens to increased interest rates, and higher prices for a range of raw materials and transportation.

Weak client demand and lower new orders led firms to scale back their hiring efforts, as employment rose at the slowest pace in 2022 to date. Although some companies continued to note challenges finding suitable replacements for voluntary leavers, a growing number of firms stated that uncertainty and rising costs led them to delay the immediate replacement of staff.

Consistent With Recession

The entire report is consistent with recession, in contrast to ISM which allegedly covers the same things.

On August 3, I reported ISM Services Smashes Estimates to the Upside, S&P Services Is Deeply Negative

Given that the S&P PMI for services weakened further, from 47.3 to 44.1, the next ISM report rates to be interesting.

Negative surprises in ISM reports tend to result in a steep dive in the Atlanta Fed GDPNow forecast.

Housing is also very consistent with recession. Note that the New Home Sales Crash Accelerates, Sales Down 12.6 Percent in July

Hello Recession Doubters

New home sales are down a whopping 38.5 percent since January!

When have we seen housing data this week when the economy was not in recession?

The S&P PMI report confirms.

previous

previous