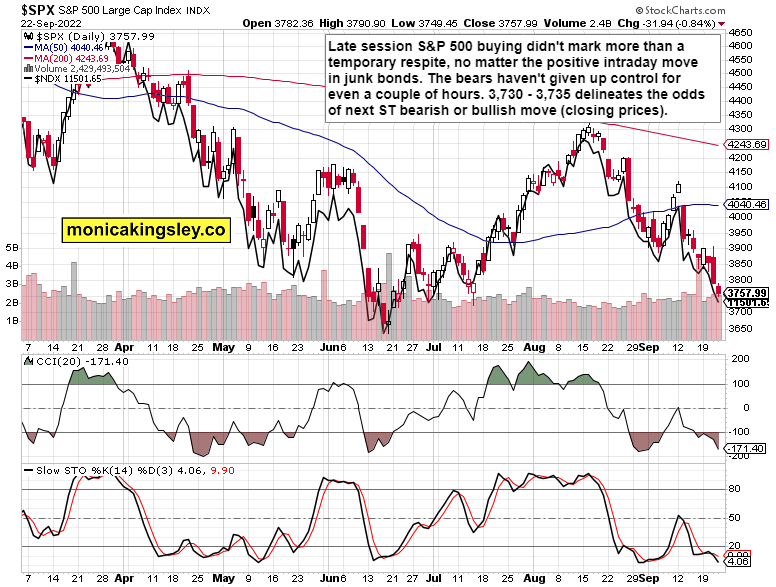

S&P 500 continued its downswing without much of a respite even though bonds favored stocks to reach higher than they did one hour before the closing bell. Interestingly, VIX has barely moved in spite of the quite meaningful downside continuation – let alone Wednesday‘s reversal that caught so many off guard. Thankfully not you!

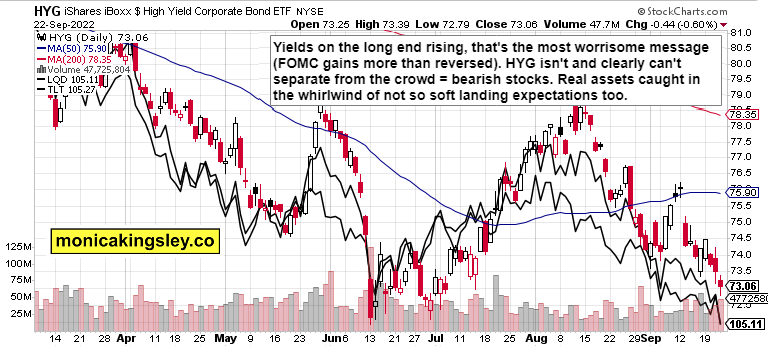

Today, we‘re already below my direction-setting level described in these two tweets. USD is up, and much of the forex antidollar plays in disarray (beyond the usual suspect, Japan) – this isn‘t yet a dollar top. That‘s a consequence of Treasuries price action – no top in yields, not enough fresh buyers to make up for the vacated Fed place, is putting and will put even more serious pressure on asset prices.

Keep enjoying the lively Twitter feed serving you all already in, which comes on top of getting the key daily analytics right into your mailbox. Plenty gets addressed there, but the analyses (whether short or long format, depending on market action – today short) over email are the bedrock, so make sure you‘re signed up for the free newsletter and that you have Twitter notifications turned on so as not to miss any tweets or replies intraday.

Let‘s move right into the charts.

S&P 500 and Nasdaq outlook

This is still a really bearish S&P 500 chart – not even volume is increasing on the downswing. Both cyclicals and tech are suffering, but the market generals (AAPL and beyond) have still quite some catching to do. After Wednesday, the selling is quite orderly still, no panic yet, but I am unwilling to chase prices here, this Friday – we‘re likely to see a temporary stabilization above 3,730, and quite possibly another buying spree approximately of yesterday‘s potency.

Credit markets

As stated yesterday, bonds are risk-off, and reflecting foremost the upcoming real economy realities, the inevitable consequence of aggressive tightening while the effects of tightening already in, haven‘t yet played out. It‘s only when TLT turns that we can get some meaningful respite in stocks beyond a few days‘ counter trend upswings here and there – in the week(s) to come.

previous

previous