- Equities fall sharply on Friday as the jobs market remains strong.

- Equities still closed higher on a volatile week, while Monday, Tuesday saw massive gains.

- Oil prices spike as OPEC+ cuts supply, all eyes now on CPI data.

Another week of huge volatility for financial markets was met with a certain resignation on Friday. Early indications for the week were positive with a massive two-day rally to set things off as the Fed pivot talk once again took centre stage. This saw a massive 6%-plus, two-day rally for most of the main indices before some flatlining ahead of Friday's jobs report. The hope was for a weak number to continue the Fed pivot hopes.

However, what we got instead were more signs of a strong labour market that will need to take a few more interest rate hits before it falls to the canvass. The unemployment rate dipped to 3.5%, while the payrolls number showed gains of 263K, just below the 270K consensus. This reinforced the hawkish comments from Fed officials, which markets had ignored earlier in the week.

Bond yields once again spiked with the 2-year closing at a yield of 4.3% and the 10-year just shy of 3.9%. Fed funds futures markets priced the near certainty of another 75bps hike in November, and as a result equities sold off aggressively. Despite all the doom and gloom the S&P 500 (SPX) actually gained 1.6%. Energy was back on its throne as the biggest winner. OPEC+ announced a 2 million barrel per day oil supply cut that sent crude oil prices spiking higher midweek toward $90. This will also not help the Fed pivot hopes. Energy (XLE) rose over 13% on the week, while the continued rate hikes meant real estate (XLRE) was the worst-performing sector on the week.

We now turn our attention to the week ahead with two key events, one micro and one macro. First, it is earnings season. Investors have been nervously anticipating this one for a while now, and as ever the banking sector is first up. We do have to question how much bad earnings news is priced in given the mess we have already seen from FedEx (FDX) and Nike (NKE) to name a few. Apple (AAPL) will be the key as in a proper full-on capitulation the leaders are the last ones to topple. If we are indeed about to capitulate, then AAPL will need to move seriously lower. On the macro front, it is all about Thursday's CPI. Another hot number would lead to curtains for the stock market. The spike in oil will not have an effect this time out, so hopes are growing for a calming number. Again though, how much is priced in?

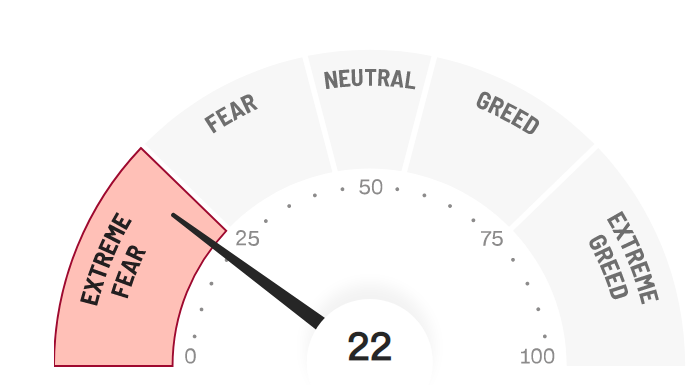

We notice the conditions for a counter-trend rally are higher than we would have expected. A number of factors support the theory. First, earnings season has arrived as mentioned. Analysts have lowered the bar with forecast downgrades, and investors largely expect a bad season. We had a similar situation in Q2, and the worst fears were not realized. Perhaps this will be more of the same. Second, positions and sentiment are again maximum bearish.

Source: CNN.com

Meanwhile, the American Association of Individual Investors Sentiment Survey is also near max bearish. Hedge funds are overly shot and could be squeezed. CTA trend-following systems are near maxed out also and will run to longs in a big way if the rally picks up. We are also close to the max period for corporate buybacks, which will soon begin to pick up again.

previous

previous