Outlook: Why did the dollar do an about-face? The comments from the Fed presidents did the trick–not the Pelosi trip, not Jolts–but even the strongest words from mere regional presidents do not usually generate this much power.

As triggers go, these are not terribly impressive. We surmise that the market really was overold and wanted to square up a bit. The move was substantial, though, and that gives us our usual trend-follower’s headache–short-lived correction or return to primary trend? We get it right about half the time.

We have push-me/pull-you risk factors today. The Pelosi trip has some still unknown after-effects making some folks nervous. Both Pelosi and Pres Biden have said the US will stand up for Taiwan, despite no defense treaty (or even diplomatic relations), and while we’d like to know why this statement and this trip at this time, we see no reason to think they are bluffing. Bloomberg opines that it’s Pelosi who gets the credit/blame. “Yields fell on the pivot narrative, but the move was amplified by concerns about Pelosi's trip to Taiwan. After her plane landed safely on the island, yields rose by over 20 basis points in a matter of hours, one of the most aggressive bond selloffs seen in five years.”

This is self-serving interpretation, not straight news. Attributing cause and effect is tricky. We can repeat that saber-rattling, even with China, hardly ever moves FX. It takes real bullets to do that.

On the other side is the idea Opec will increase output. The FT writes “Saudi Arabia is moving towards a push for a small increase in oil production when the Opec+ group meets later on Wednesday, as it looks to bolster an improvement in relations with western powers in recent weeks.

“Four people briefed on the kingdom’s thinking said a small production increase was becoming the most likely outcome in the wake of Crown Prince Mohammed bin Salman’s welcome in France last week and following US president Joe Biden’s trip to Jeddah in July.”

Risk appetite should be returning. We even have revisions to final PMI’s in Europe showing conditions less bad than in the flash. Whether this pushes back against the dollar’s gain and makes it a one-day wonder remains to be seen.

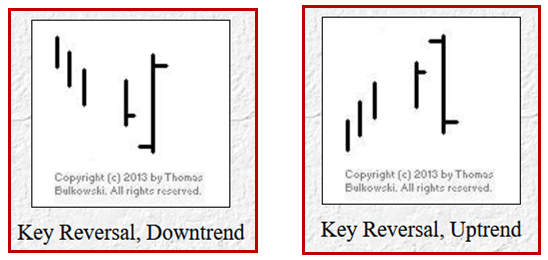

Some analysts are making a big deal out of the bar pattern, known as an outside day (higher high and lower low than the day before) and also as a key reversal. Considering that the usual timeframe for trading FX is not the daily basis (but rather 60-240 minutes), we have our doubts about whether the classic bars and candlesticks retain their traditional meaning.

In any case, if you want the real scoop on patterns, there is only one source–The Pattern Site. Author Bulkowski, who wrote the definitive books, gives you incidence and outcomes in mind-numbing detail. The data is all for equities, but never mind–human behavior is the same or at least similar no matter the asset class. And since everyone sees the key reversal, we should talk about it.

Do not consult YouTube or other sources. That’s because they all consider the key reversal to be a one-day phenomenon and it’s not–it takes two. The close in an upside key reversal has to hold the high for a second day to deliver the bullish promise. The same thing holds for the bearish version, which is what we have in the euro.

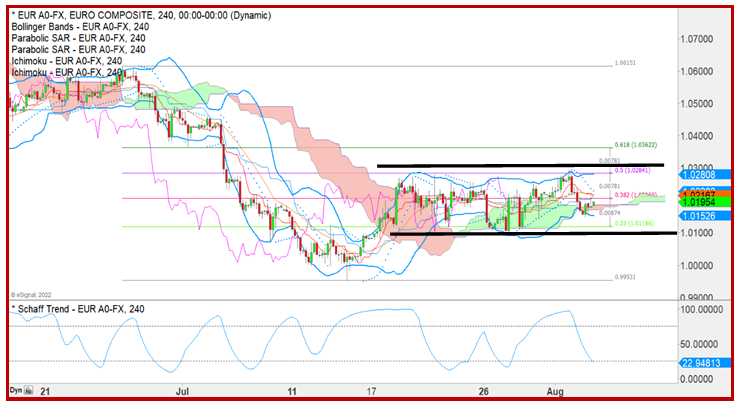

Now consider scale. On 8/1, the euro high was 1.0275. Yesterday, the high was only 19 points higher (1.0294), which in an average true range of about 150 points is a mere 13%. We want to see a higher high so that the end result, a vastly lower low, appears vastly lower. Then there’s that second day criterion. For the reversal to be “key,” is has to last more than one day. This seems too obvious for words.

Also pretty obvious has to be confirmation by another independent indicator. It can be one of the channels/bands or something like relative strength/momentum. You can get a band/channel breakout in a day but that’s too quick for most indicators and certainly our best one in FX, the MACD. Finally, confirmation can come from another security but can also be a trap. We have a clear, big reversal in some other places, notably the dollar/yen. But again, one day does not a reversal make.

Finally, context matters. See the 240-minute euro chart. We are still within a range and that range is still is within the 23-50% retracement zone. Key reversal is not proven. We sometimes choose to pretend to buy into the consensus view for a quick gain but other times we stick to our knitting. As noted above, we are right only half the time. This time we expect divergence in the dollar vs. various other currencies, including the yen and pound. The big worry is the AUD–it fell too much. The CAD is absolutely no help at all, either.

Don’t count chickens.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

previous

previous